When it comes to managing your finances, taxes are an unavoidable expense. However, there are ways to reduce your tax burden and increase your savings.

Here are five tax savings tips to help you keep more money in your pocket:

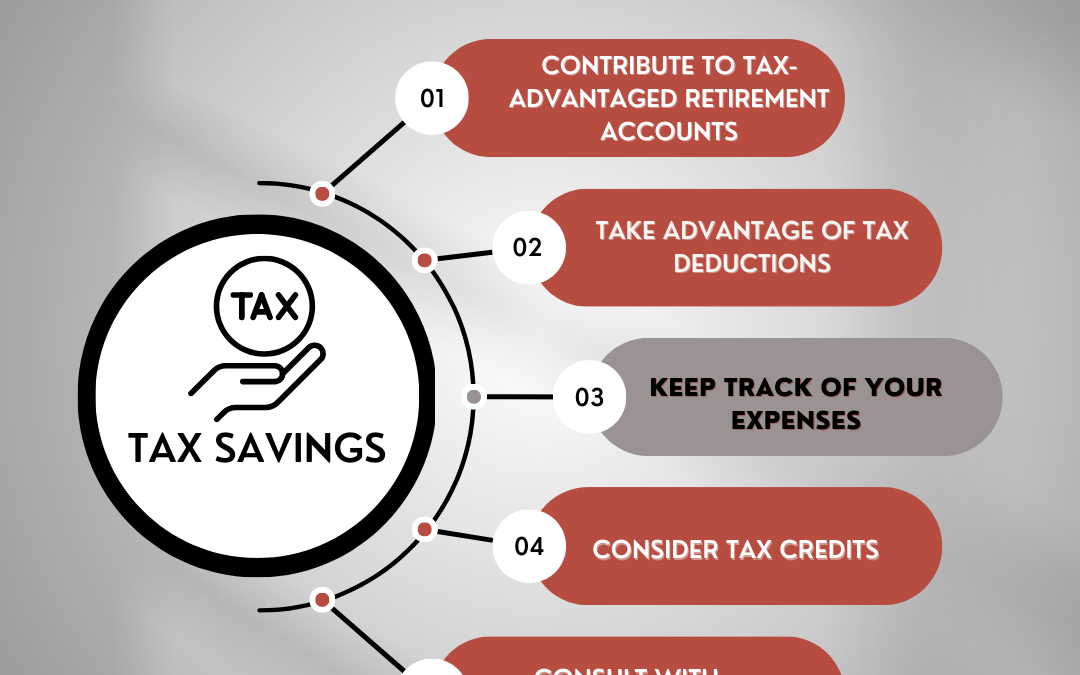

Contribute to tax-advantaged retirement accounts

One of the most effective ways to reduce your tax bill is by contributing to a tax-advantaged retirement account, such as a 401(k) or IRA. These accounts provide an excellent opportunity to save for your retirement while simultaneously lowering your taxable income. By contributing pre-tax dollars to your retirement account, you can reduce your tax bill in the current year, allowing you to retain more of your income. Additionally, many employers offer matching contributions, which can significantly boost your savings and help you achieve your long-term financial goals.

Take advantage of tax deductions

Tax deductions allow you to subtract qualifying expenses from your taxable income, reducing the amount of taxes you owe. Some common deductions include mortgage interest, charitable donations, and medical expenses. However, to take advantage of these deductions, you’ll need to itemize your deductions instead of taking the standard deduction. It’s important to keep detailed records of your expenses throughout the year so that you can claim all eligible deductions and maximize your tax savings.

Keep track of your expenses

Keeping track of your expenses is essential to effective tax planning. By maintaining organized and detailed records of your income and expenses throughout the year, you can identify areas where you may be overspending or missing out on opportunities to save. This information can help you make informed decisions about your finances and optimize your tax strategy.

Consider tax credits

Tax credits provide a dollar-for-dollar reduction in taxes owed, making them even more valuable than deductions. Some common tax credits include the child tax credit, earned income tax credit, and education credits. However, each credit has specific requirements and limitations, so it’s essential to understand which ones you qualify for and how to claim them. By taking advantage of tax credits, you can significantly reduce your tax bill and keep more of your hard-earned money.

Consult with ACCOUNTING BW

Finally, working with ACCOUNTING BW can provide invaluable assistance in optimizing your tax strategy. An experienced accountant can help you identify opportunities to reduce your tax burden, stay compliant with tax laws and regulations, and provide valuable insights into your financial health. Additionally, they can assist with tax planning throughout the year, so you can make informed decisions and stay on track with your financial goals.

In summary, taxes are an integral part of our financial lives, and taking the time to optimize our tax strategy can yield significant benefits. The five tax savings tips we’ve discussed – contributing to tax-advantaged retirement accounts, taking advantage of tax deductions, keeping track of your expenses, considering tax credits, and consulting with us are all powerful tools that can help you reduce your tax bill and maximize your savings.

While implementing these strategies may require some effort and diligence, the long-term benefits are well worth it. By reducing your tax burden, you can keep more of your hard-earned money, build a stronger financial foundation, and achieve your long-term financial goals more quickly. Moreover, working with us can provide you with the guidance and expertise you need to make informed decisions and stay on track with your financial plans.

So, as you navigate the world of taxes, remember that you are not alone. With the right tools and resources at your disposal, you can take control of your finances and achieve the financial success you deserve. So, take the first step today and start implementing these tax savings tips, and watch your financial future flourish!